This blog was published by the Center for Global Development (CGDEV).

Realizing the Sustainable Development Goals (SDGs) and tackling the climate crisis in developing nations demands substantial investments. A recent report commissioned by the G20 estimated that for developing countries (encompassing low-income, lower-middle-income, and upper-middle-income nations), approximately two-thirds of their annual financing must come from domestic resource mobilization and local finance, with the remaining portion originating from external sources. An IMF study in 2019 found that, on average, low-income developing countries would need to increase their domestic revenues by an additional 5 percent of GDP to finance the SDGs. Since then, funding needs have escalated due to the impact of COVID-19 and the investments needed for the climate transition.

While developing countries have made progress in augmenting their domestic tax revenues in the past three decades, with an average increase of 3 to 5 percent of GDP, many low-income developing nations have not yet reached the necessary taxation levels to sustain their development.

This blog post contends that one avenue for developing countries to enhance their local resource generation is through the reform of tax expenditures. Unfortunately, advanced countries do not provide a model worthy of emulation by developing nations.

Tax potential in developing countries

A recent IMF paper has estimated that if developing countries increased their tax efforts and realized their “revenue potential,” they would raise additional revenues of between 5 and 9 percent of GDP. Nevertheless, this transformation would be gradual, as it will take time for countries to fortify their tax systems, strengthen fiscal institutions, and enhance tax compliance. Experience reveals that overhauling tax systems is a formidable challenge due to resistance from entrenched interests.

Understanding tax expenditures

One significant area identified by the IMF study as a source of revenue loss in developing nations is tax expenditures. Tax expenditures encompass benefits accorded to specific sectors, activities, or groups through preferential tax treatments, such as exemptions, deductions, credits, deferrals, and reduced tax rates. Governments utilize tax expenditures to stimulate economic growth, improve social welfare, attract investments, and promote the adoption of renewable energy. These expenditures generally undergo less scrutiny in budgetary processes compared to direct spending and are infrequently evaluated in terms of their costs and benefits. Consequently, they are almost like an “off-budget” expenditure. Tax expenditures are particularly pervasive in value-added tax and corporate income tax regimes.

Tax expenditures in advanced economies

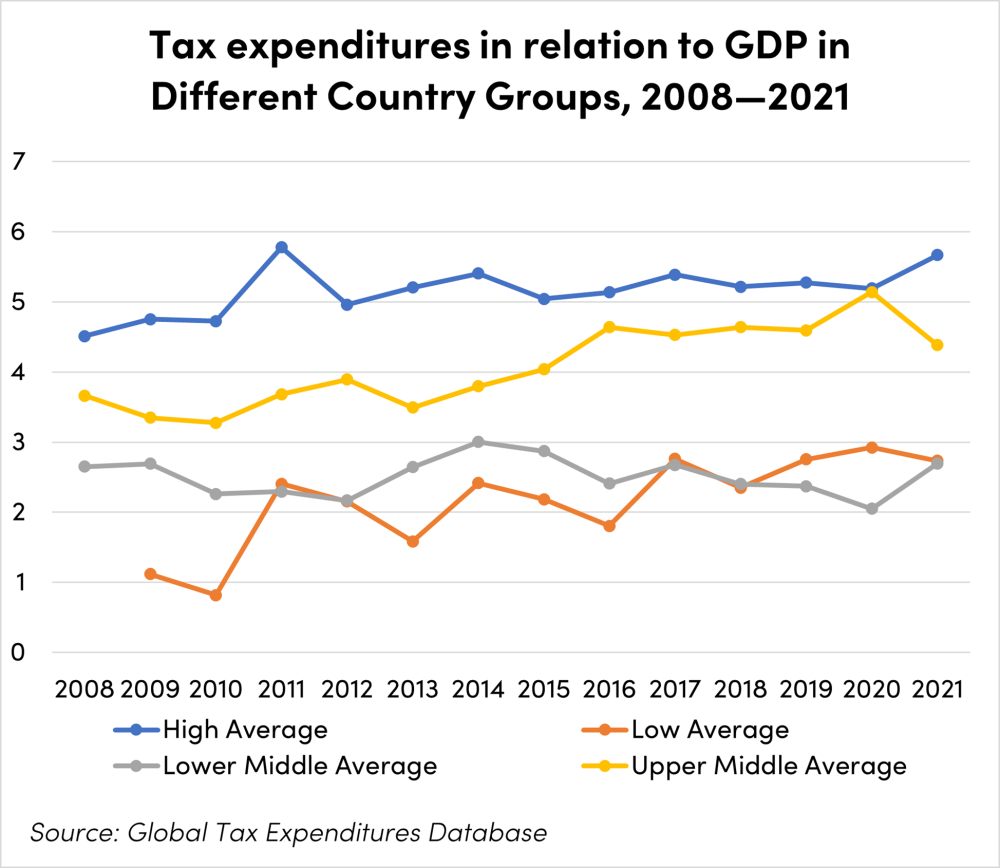

What is intriguing is that the average cost of tax expenditures in advanced economies is over twice that of low-income countries (as depicted in the figure below). This estimate should be treated with caution as not all advanced (as well as low-income, and low- and upper middle income) countries report their tax expenditures. The tax expenditure database is constructed from reports from 105 countries, while 113 are still not reporting.

One might argue that average cost of tax expenditures in advanced countries is higher because they exhibit greater transparency regarding exemptions and tax concessions granted to various consumers and producers. A recently launched Global Tax Expenditure Transparency Index covering five dimensions estimates an average transparency score of 48 on a scale of 100 for countries, which is rather low. Interestingly, Japan’s ranking is below that of Liberia and Mongolia, and Denmark, Finland, and Switzerland are lower than Honduras in terms of transparency.

This does not augur well for developing countries. How can the international community convince developing countries to curtail tax expenditures, to enhance local resource mobilization to cover their share of SDGs and climate transition financing, when advanced countries are continuing to “spend” so much more on tax expenditures, with many not reporting or being fully transparent about them?

I wish to thank Benedict Clements and Agustin Redonda for helpful comments on an earlier draft.