This blog was first published by Sofia Berg, Research Analyst at the Council on Economic Policies.

Tax expenditures, i.e. benefits granted through the tax system, do not exist in a political vacuum. They are an outcome of political deliberations, and reforms can often be the focus of intense debate. Therefore, the role of parliamentarians should be well established at each stage of the tax expenditure policy cycle. This is crucial to increase accountability and transparency within the tax expenditure field and, at the same time, to ensure that the decision-making processes are based on evidence and sound information. Whereas specific roles and functions of parliamentarians can vary from jurisdiction to jurisdiction and depend on country-specific systems and institutions, there is a broad consensus about the need for parliamentarians to be key actors in tax expenditure policymaking.

Against this background, my co-authors and I, in collaboration with the Addis Tax Initiative (ATI), recently launched the Pocket Guide on Tax Expenditures for Parliamentarians. The document lays out concrete intervention points for parliamentarians along the tax expenditure policy cycle.

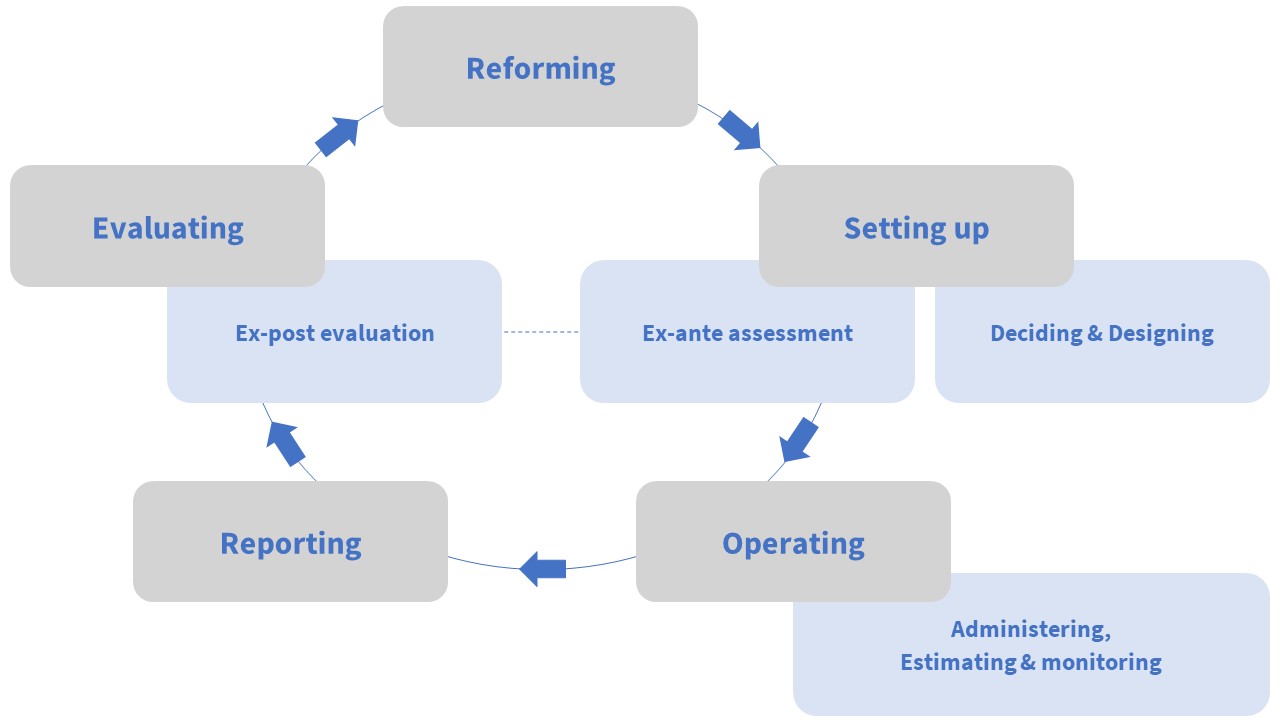

The tax expenditures policy cycle – from setting up to reforming tax expenditures

The tax expenditure policy cycle illustrates different aspects of tax expenditure policymaking, highlighting the interconnections between political decision-making, administrative implementation, and policy evaluation. It consists of five stages covering the setting up of new tax expenditure provisions as well as the operating, reporting, evaluation, and reform of tax expenditures already in place (see Figure 1). What is done or decided in one stage has implications for the procedures and outcomes of later stages.

Figure 1. The Tax Expenditure Policy Cycle

To begin with, setting up tax expenditures involves decisions to introduce new tax expenditures as well as design features of individual provisions. This stage also highlights the necessity of carrying out ex-ante assessments, which are essential to rationalize the introduction of tax expenditures by assessing their potential impact and externalities. Operating concerns the administration, estimation, and monitoring of tax expenditures. Regular and comprehensive reporting is essential for well-informed and evidence-based policymaking. Evaluating refers to in-depth assessments of existing tax expenditures (i.e. ex-post evaluations), which, as a minimum requirement, should contain a cost-benefit analysis. Evaluation results should provide insights about the need and ways to reform (e.g. modify or dismantle) tax expenditures.

The role of parliamentarians

Today, many governments face an urgent need to rationalize the use of tax expenditures due to rising levels of indebtedness and shrinking fiscal space. This is especially critical as evidence on the effectiveness of tax expenditures is, at best, mixed. In navigating this complex landscape, the role of parliamentarians is, and should rightfully be, at the heart of the rationalization process.

Tax expenditure policy involves several actors and institutions, for example, the ministry of finance, the revenue authority, and national audit offices. Consequently, it should be based on a sound and transparent legal framework, including a clear definition of responsibilities and explicit rules on inter-agency cooperation and exchange of information (data sharing protocols). Parliaments should be the main actors in establishing such a governance framework and should regularly be informed on the use of tax expenditures. Indeed, their role is vital with regard to the monitoring and control of tax expenditures, both as part of the regular budget cycle and ad hoc, if required.

As the legislative body representing the people, the parliament should be the authority approving new tax expenditures or reforming existing ones. To fulfil this function, parliamentarians need to receive exhaustive and detailed information at the individual tax expenditure provision level, including estimates of their fiscal cost (i.e. revenue forgone), policy goals and beneficiaries. Likewise, annual tax expenditure reports, ex-ante assessments, and ex-post evaluations should serve as primary inputs to guide evidence-based policymaking. All the information should be presented to the parliament in a timely manner, where tax expenditure reports should be aligned with the annual budget cycle. The parliament should also play a crucial role in setting up a binding evaluation framework to establish what is evaluated, by whom, when, and how the results and main takeaways of evaluations are fed back into policymaking. Unlike tax expenditure reports, it is not feasible or necessary to perform evaluations of all tax expenditures on an annual basis. Rather, a multiyear evaluation cycle is the way to go.

By definition, tax expenditures provide preferential tax treatment to specific groups of taxpayers, making the political economy behind policymaking a key aspect to consider. Against this background, parliamentarians often face pressure from interest groups, specifically from those affected by the related policy decision. A case in point is when the Dutch parliament, in 2022, proposed to remove the reduced excise tax rate for small breweries. The tax incentive was introduced in the old tax system, before 1992, with the objective to adjust for smaller breweries facing a higher effective rate than larger breweries under a uniform rate. When the tax system changed in 1992, the reduced rate was maintained despite the rationale of it being lost. The tax expenditure was deemed ineffective by a 2008 evaluation, and the government later proposed to abolish it in the 2022 budget. When the budget bill was debated in parliament, the reform met strong pushback fuelled by lobbying from small breweries. Consequently, this led to a reversal of the proposed reform and the reduced rate kept in place. The considerable resistance the abolishment faced illustrates the complexity of tax expenditure reform and the challenges of dismantling provisions once they have been introduced, even in cases when there is empirical evidence against the tax expenditure under scrutiny or when the rationale of the provision has since long disappeared.

Understanding the long-term effects on society and basing the political debate on evidence is vital to legitimise tax expenditure reforms. Communication is another crucial element of any tax expenditure policy decision, where transparency should serve as the guiding principle. Indeed, communication is vital to managing the expectations of interest groups likely to be affected by the policy or reform in question, serving as the link between the political debate within the parliament and the public debate at the societal level. Lastly, the entire tax context should be considered when reforming tax expenditures. Sometimes, tax expenditure provisions interact with each other or have been implemented to compensate for or offset the negative effects of other policy measures. Thus, a holistic approach to tax expenditure reform is not only critical from a technical perspective but is also likely to increase the likelihood of success of the reform process.

Download the Pocket Guide.