To address the COVID-19 pandemic, numerous countries have adopted accommodating tax policies, providing deferrals, credits, reductions, and even tax exemptions. Beyond this crisis, financial liberalization triggered a downward tax competition among countries. Tax competition may take several forms, such as the decrease in statutory tax rates, especially for Corporate Income Tax (CIT), narrower taxable base resulting from additional deductible costs as allowance for corporate equity or accelerated depreciation rules, or tax credits[1] for multiple purposes (research and development, employment, green transition, etc.). A particular tax incentive is CIT exemption (or equivalently, CIT holidays), which is common in developing countries. The Global Tax Expenditures Database (GTED) identifies 1,613 CIT exemptions in 101 countries (see Redonda et al., 2021).

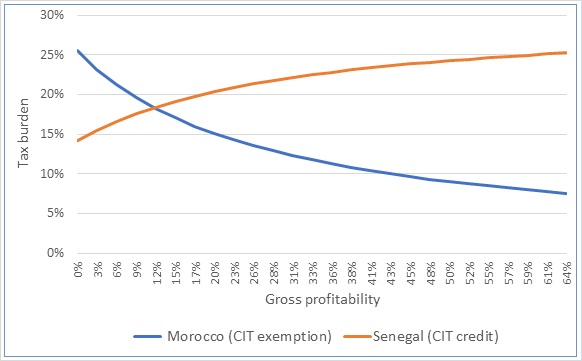

In a recent article (Dama et al., 2023), we establish the regressivity, thus the redundancy and inconsistency of CIT exemptions, based on the extent up to which these Tax Expenditures (TEs) tend to favor more the most profitable companies (regressivity), and equivalently firms that would have invested without these incentives (redundancy and inconsistency). Following Djankov et al. (2010) and, more broadly, the Doing Business report approach,[2] we compute a representative firm’s Effective Average Tax Rate (EATR) with and without investment tax incentives. We study the progressivity of the tax burden by varying the pre-tax profitability of the company in 44 African countries in 2020. A tax regime is progressive (regressive) when the tax burden increases (decreases) in the pre-tax profit. The cases of Morocco and Senegal are cases in point (Fig. 1). For example, whereas a Moroccan company with a 10 percent gross margin faces a tax burden of 18 percent under the Moroccan Investment Code (IC), the tax burden for a company with a 30 percent gross margin is significantly lower (about 13 percent). Of the 44 African countries studied, 20 have a regressive IC. Our analysis is replicable on the dedicated website: https://shiny.mesocentre.uca.fr/app/citregressivity

Besides the impact on the regressivity of the tax burden, CIT credits have several advantages with respect to CIT holidays. First, credits involve a more limited tax expenditure (revenue forgone) since the tax base corresponds to a share of eligible investment. Secondly, tax credits improve unambiguously the targeting property of tax incentive mechanisms since they address directly relevant investments. CIT exemptions instead, benefit firms and not specific investments. Thirdly, tax credits are more transparent than CIT exemptions. The former require information disclosure after investments are completed or at least partly made, while CIT exemptions are generally provided based on statements of investments’ intents only. Fourthly, replacing CIT exemptions with CIT credits would also transfer the burden of the proof from the Investment Promotion Agency (IPA) or the tax administration to beneficiary firms since the latter would have to claim their tax credits when they file their CIT returns. Finally, tax credits reinforce the Ministry of Finance’s (MoF) taxing power, given the central role of the tax administration in monitoring this type of tax incentive.[3] Indeed, IPAs generally report to other Ministries or even the Prime Minister’s office.[4] These institutional frameworks affect the supervisory role of the MoF on economic agents[5] requiring a reinforcement of intra-governmental coordination, which is often lacking in developing countries.

Figure 1: Tax burden in Morocco and in Senegal: CIT holidays vs CIT credit

[1] We consider tax credits as mechanisms that reduce the amount of taxable income (and tax due) depending on investment. For instance, a firm invests in some capital goods eligible for tax credit. This investment would generate depreciation allowances that reduce taxable profit and the right to decrease taxable profit by a percentage of the eligible investment. Tax credits are refundable in our country sample.

[2] The World Bank Group adopted this approach to compute some indicators in its yearly Doing Business survey.

[3] From the GTED database, CIT expenditures are more important in countries with a CIT credit mechanism than in countries offering CIT exemptions. This observation may appear counter-intuitive. However, it is an illustration of another weakness of the CIT exemption mechanism: The lack of accurate information and effective monitoring of eligible firms by the tax administration. This incentive involves a high risk of fraud or abuse and significant complexities in monitoring and evaluating induced tax expenditures.

[4] From a joint survey conducted by the World Bank Group (WBG) and the World Association of Investment Promotion Agency (WAIPA), 32 percent of API report to the Ministry of Industry and/or Commerce, 14 percent to the Prime Minister’s Office, and only 4 percent to the Ministry of finance (see Sanchiz and Omic, 2020).

[5] In some countries, such as Madagascar, the API provides Tax Identification Numbers to eligible firms without automatically exchanging information with the tax administration.

References:

Dama, Alou Adessé, Rota-Graziosi, Grégoire et Fayçal Sawadogo, 2023, “The Regressivity of CIT Exemptions in Africa,’’ International Tax and Public Finance, December, https://doi.org/10.1007/s10797-023-09825-6

Redonda, A., von Haldenwang, C., and F. Aliu, (2021). The Global Tax Expenditures Database (GTED). https://gted.net/2021/05/the-global-tax-expenditures-database-companion-paper/

Sanchiz, A., and A. Omic. (2020). State of Investment Promotion Agencies: Evidence from WAIPA-WBG’s Joint Global Survey. Washington, DC: World Bank.

This blog was writen by Alou Adessé Dama,1, 2,3 Grégoire Rota-Graziosi1, 2 et Fayçal Sawadogo1, 2,4

1 Université Clermont Auvergne, CNRS, IRD, CERDI, F-63000 Clermont-Ferrand, France

2 Fondation pour les Etudes et Recherches sur le Développement International (FERDI), F-63000 Clermont-Ferrand, France

2 Faculté des Sciences Economiques et de Gestion (FSEG), Université des Sciences Sociales et de Gestion de Bamako (USSGB), Bamako, Mali

4 Fiscal Affairs Department, International Monetary Fund