This Report was published by the National Audit Office (NAO).

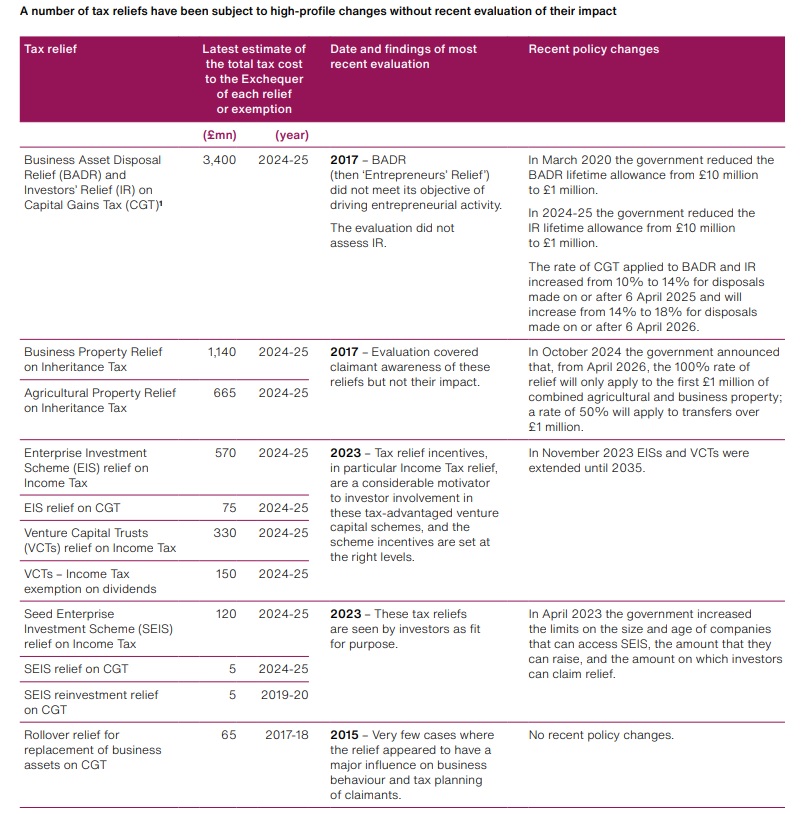

“Taxpayers can use a range of tax reliefs to reduce their tax liabilities. For personal taxes, there are around 200 ‘non-structural’ reliefs, designed to reduce the tax burden on particular groups or sectors, encourage a particular behaviour or serve a social purpose. For the majority of these reliefs, HMRC has published either no estimate of the tax cost to the Exchequer of the relief, or only older, single-year estimates, though its coverage is improving. Figure 1 on pages 17 and 18 of the report shows 12 reliefs that are likely to be extensively claimed by wealthy individuals and on which costs HMRC does publish information … HMRC commissions evaluations of some reliefs to provide evidence for how well reliefs are meeting their objectives. We reported in January 2024 that evaluations can contribute to changes that save billions of pounds for the Exchequer. While HMRC has published an evaluation for all 12 reliefs we investigated, some tax reliefs subject to recent and significant policy change have not been evaluated for some time or sufficiently to understand the benefits (Figure 1) … Wealthy individuals often rely on the expertise of a tax agent to help them organise their finances and investments in a tax-efficient way, interpret how to apply complex tax rules and reliefs and file accurate returns. Some 73% of wealthy individuals (more than 600,000 people) are represented by an agent. HMRC has limited direct engagement with many wealthy individuals and, instead, engages with the taxpayer’s agent.”

Figure 1 – Examples of tax reliefs claimed by wealthy individuals

Notes

1 HMRC does not report separate cost estimates for BADR and IR.

2 The reliefs covered in this figure represent a subset of all tax reliefs that are available to wealthy individuals.

3 Since 2019-20, HM Revenue & Customs (HMRC) defi nes wealthy individuals as those who have incomes

of £200,000 or more, or assets equal to or above £2 million, in any of the last three years.

4 Cost estimates are from HMRC’s December 2024 publication.

5 HMRC’s tax relief evaluations are either carried out by HMRC analysts or commissioned from external organisations.

In general, evaluations aim to determine if reliefs are achieving their stated objectives.

Source: National Audit Office analysis of HM Revenue & Customs data

© National Audit Office, 2025

Read the full report HERE