Tax expenditures (TEs) are less well understood in Sub-Saharan Africa (SSA) than in other regions, and deserve closer attention given the region’s macro-fiscal challenges. A new IMF paper shed some additional light on TEs in SSA, their potential importance to domestic revenue mobilization, and offers a roadmap for reform.

TEs are found in many countries regardless of region or level of development. They frequently take the form of tax incentives for firms, tax deductions for households, and reduced tax rates for specific goods and services. As implicit forms of government support, TEs represent a significant, but often opaque, component of fiscal policy. Unlike direct government spending lines, TEs are rarely subject to the same level of scrutiny during the budget process and are seldom assessed (or reassessed) in terms of their costs and benefits.

Without credible reporting and oversight, TEs can also undermine governance—enabling nontransparent and preferential treatment for selected groups and increasing the risk of abuse and corruption.

The IMF has been addressing TEs in its engagement with Sub-Saharan Africa—recognizing the scope to enhance revenue mobilization and create space to reduce poverty and inequality, finance other development goals, and boost transparency and governance. Given the current challenges around elevated public debt, tighter external financing constraints, and rising spending needs, the paper argues that policymakers in the region should take steps to advance TE reforms.

Tax Expenditures in Sub-Saharan Africa – an Uneven Landscape

The knowledge base on TEs in SSA has grown in recent decades. However, there is still considerable variation in how countries report and manage TEs. A survey of IMF mission teams working on SSA countries—complementing existing knowledge based on publicly available TEs (e.g. the GTED)— reveals significant gaps in those areas:

- About 30 percent of SSA countries do not have an inventory of TEs, or an estimate of revenue forgone from these measures.

- Among the other 32 countries that do report, only about half of TE reports are comprehensive and published. The absence of a full estimate of revenue forgone in the other half could likely be improved through a rigorous assessment based on a benchmark tax system.

- Publication of TE estimates—essential to ensure transparency and assess their success or failure relative to stated objectives—varies across SSA countries. Roughly one-third of SSA countries with TE estimates choose not to publish them.

- Governance of TEs also varies. About one quarter of SSA countries reporting TE estimates appear to lack legislative rules governing TEs. An even larger share do not have a single authority, such as the finance ministry, that oversees TEs.

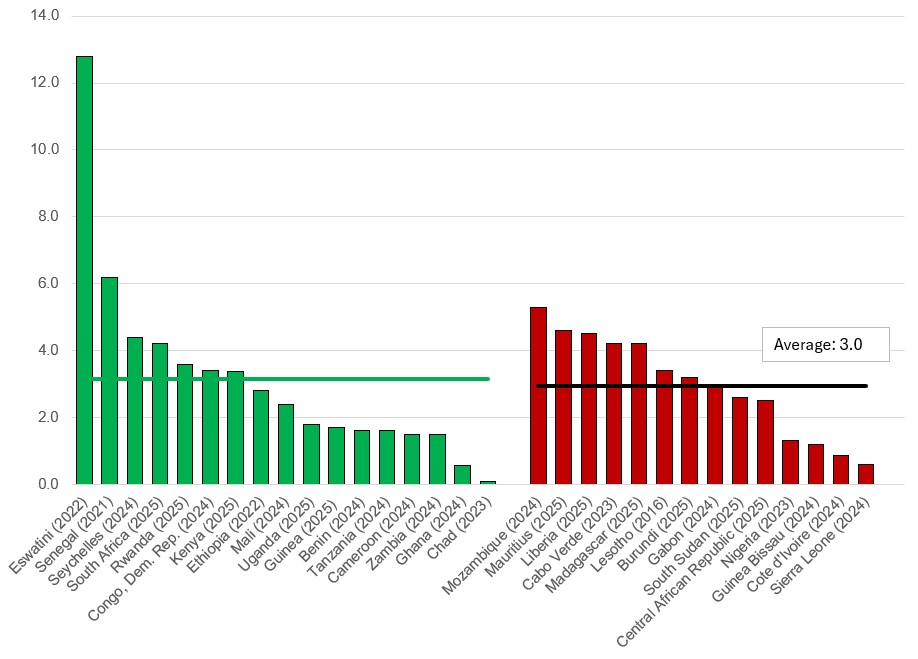

These variations in reporting, publishing, and oversight highlight the uneven terrain of TEs in the region but also their potential importance to policymakers and stakeholders. The macroeconomic importance of TEs in the region also appears clear. Estimates of the cost of TEs vary considerably given the complexities involved in their estimation. But a snapshot across countries where at least some data is available suggests that revenue forgone ranges from 0.1 percent to 13 percent of GDP—averaging about 3 percent of GDP across all reporting countries. TEs in the value-added tax and corporate income tax frameworks appear to be the major driver of this forgone revenue in the region.

Figure 1. Estimated Cost of Tax Expenditures (year of latest report)

Sources: IMF Staff Calculations, AFR Mission Chiefs TEs in SSA Survey, 2025. Percent of GDP, green indicates full estimate, red is partial estimate.

IMF Efforts to Address Tax Expenditures in Sub-Saharan Africa

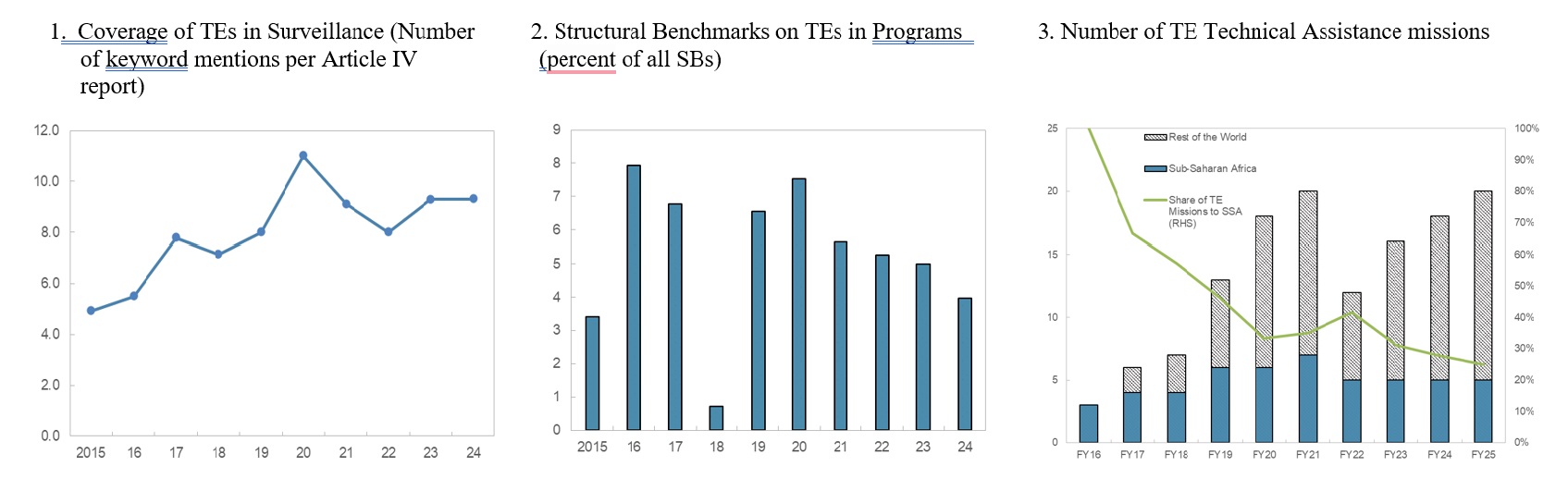

Analyzing TEs, assessing their revenue impact, and proposing reforms in line with sustainable medium-term fiscal frameworks lie at the heart of the IMF’s mandate and core expertise. A review of IMF engagement in the region confirms that TEs have been a prominent concern for the IMF—featuring in regular member-country surveillance, program engagement, and capacity development (technical assistance) activities.

Figure 2. IMF Engagement on Tax Expenditures, 2015-24

Sources: IMF Article IV Staff Reports; IMF Technical Assistance Reports; IMF staff calculations.

Sources: IMF Article IV Staff Reports; IMF Technical Assistance Reports; IMF staff calculations.

The IMF’s focus on TEs in surveillance appears to have increased since 2020, reflecting a broader push for domestic revenue mobilization across the region. This is mirrored in the more frequent inclusion of structural reforms related to TEs in IMF-supported programs since 2015, alongside extensive technical assistance and capacity development in this area.

The current context of tight liquidity, declining external aid flows, and rising spending needs reinforces the need for SSA countries to look to domestic revenue mobilization and bring greater scrutiny to TEs. More could potentially be done in partnership with member countries and key stakeholders (including other international financial institutions) to advance TE reforms and strengthen fiscal resilience.

Developing a Roadmap for Reform

Assessing TEs is not a simple task. It requires administrative capacity, timely access to tax records, and specialized expertise—items frequently in short supply. Establishing a sound benchmark tax system—essential for estimating revenue forgone through TEs—can be a daunting exercise for many countries in the region, which may help explain the large reporting gaps in Sub-Saharan Africa.

On the positive side, the body of accumulated knowledge on TEs is deep—built up over six decades of practice in a broad range of countries and among key international organizations including the IMF, OECD, and World Bank.

Though potentially daunting, establishing a TE policy framework and integrating revenue costs into fiscal planning are achievable, as demonstrated by a growing number of SSA countries. Some prominent success stories are highlighted in the paper, for example:

- The Gambia is advancing, with IMF support, to broaden TE reporting and costing, including domestic TEs beyond imported concessions.

- Uganda is making significant progress in TE reporting and reform (with assistance from the IMF and World Bank) with a view to boosting revenue as well as enhancing economic efficiency and growth.

- The Democratic Republic of Congo has integrated TE reporting into its budget process. Despite challenges related to data gaps and limited capacity, starting the TE report with imperfect data and leveraging available information to improve policy has been key to getting the process rolling. Current reforms focus on eliminating and reforming major TEs.

Systematic identification and costing of TEs, though a valuable first step in the process, is not a silver bullet for the region’s financing needs. Critically, policymakers should be prepared to act on this information—reducing or eliminating TEs where costs exceed benefits and applying scrutiny and a legal framework to the granting of new measures—taking note of case studies in the region. A roadmap to this end could include the following considerations:

- Mandating TE assessments (ex-ante and ex-post) and incorporating these as part of the budget process.

- Undertaking a partial assessment with imperfect data and simple methods is better than no assessment at all. Such preliminary assessments can be used as a policy tool and can serve as a stepping stone to a more rigorous inventory and costing of TEs.

- Leveraging external expertise through training and technical assistance, and making use of existing guidance and tools from international financial institutions (IMF, World Bank, OECD).

- Pursuing regional coordination, including regional directives that lay out best practices in TEs and facilitate information exchange, which can help discipline national TEs. Basic training and workshops at the regional level can facilitate peer learning, help address common challenges, and streamline TEs at the regional level.