This article was first published in the author’s blog How to tax it and spend it

The Tánaiste and Minister for Finance Simon Harris gave an interview to RTÉ radio last weekend that I found exasperating. It wasn’t just his attempts to paint the very belated publication of a loose medium term fiscal plan as somehow rooted in a prudent approach to the public finances. Nor his “we’re definitely serious this time” commitment to stopping departmental spending overruns.

Rather, it was the floating of yet another tax break: this time for savings.

A tax break for the ‘squeeze-middle’?

I found this exasperating, firstly, because the Tánaiste tried to justify the idea as aimed at helping “the squeezed middle who are putting money in the post office or the credit union”, pointing to an astonishing “€170 billion euro on deposit in Ireland”.

This refers to frequently cited Central Bank figures on the amount held by households as deposits in Irish resident credit institutions, of which ~€74 billion is in current accounts (see Table A.11.1 here). Given there are about 1.8 million households in Ireland, that equates to an average of almost €95,000 in deposits – and €41,000 in current accounts – per household.

If that sounds implausibly high it’s because it is. As this guidance note outlines, what the Central Bank refer to as households here also includes “sole proprietorships and partnerships without independent legal status” as well as “Non-profit institutions serving households (NPISHs)”. This latter group contains “sports clubs, unions, churches, charities helping the poor and similar bodies”. So don’t worry, your family is not some atypical example of profligacy if you don’t have €40k sitting in your current account.

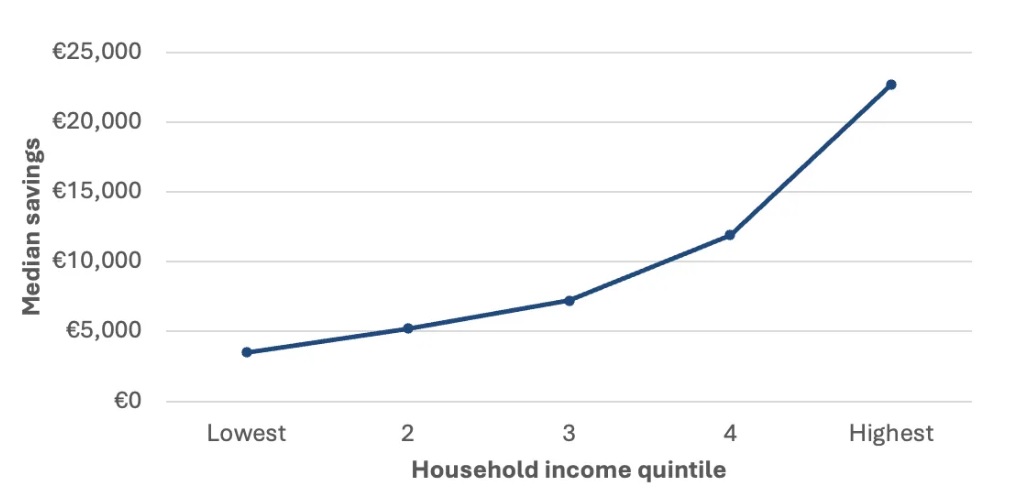

What do households – as more colloquially defined – actually hold in savings? The best data we have on this comes from the ECB led Household Finance and Consumption Survey (HFCS). CSO analysis of this survey suggests that in 2023, 98% of households held some money in either a current or a savings accounts with a median value of €8,700 (down from €9,700 in 2020).

Unsurprisingly, the HFCS also shows that these deposits are not held equallyThe Figure below based on the data published by the CSO plots the median value held in current or savings accounts across fifths (aka quintiles) of the income distribution. It may not surprise you that there is a sharp gradient, with the median rising from €3,500 for the lowest-income fifth of households to €22,700 for the highest-income fifth of households.

Source: https://data.cso.ie/table/HFC2003

Courting household deposits with tax breaks is therefore inevitably going to amount to tax cuts for the highest-income households who hold lots of deposits, not the “squeezed middle” who – however tortiously defined – don’t have a whole lot of deposits crying out to be invested.

Tax breaks for savings are also unlikely to be effective at achieving another objective the Tánaiste set out: “helping incentivise savings and investment”. That’s because there is just not very strong evidence that tax breaks for savings actually generate much additional savings. For example, a famous 2014 paper by Chetty et al. found that every 100 euro spent on tax subsidies for retirement saving in Denmark generated just 1 euro in additional savings: not exactly a great return…

And this is not an isolated finding. As John Friedman described it in his review of the literature, the evidence we have suggests that “tax subsidies appear to primarily affect the allocation of savings across accounts, rather than the total amount of savings”. That’s because households who are already saving will – if they have any sense (or financial advice) – just redirect existing savings into the new tax favoured vehicle.

Imagine if later this year in his first Budget the Minister for Finance introduced a new tax-free account for savings invested in mutual funds. Before the day was out, accountants up and down the breadth of the country would be in touch with their clients advising them to sell stakes in mutual funds they already hold and re-purchase them through this new, tax-efficient savings vehicle. The net effect on savings and investment? Next to nothing, but at substantial cost to the exchequer that will rise rapidly.

In short, the new savings tax breaks floated by the Tánaiste will do little to increase savings and investment, but instead just benefit existing higher-income savers along with their accountants and banks (whose lobby group just so happened to propose such tax breaks last week).

We tax savings badly … this won’t fix it

The other reason I found the Tánaiste’s floating of new savings tax breaks so exasperating is because there are genuine problems with how we tax savings. But these are not so much about the tax system discouraging savings as distorting them.

Our system primarily does this by bestowing enormous tax advantages on particular types of saving, including:

- Owner-occupied housing, most notably through the exception of any increases in property prices from Capital Gains Tax through principal private residence relief.

- Owner-managed businesses, through revised entrepreneur relief, retirement relief and – if one is intending on gifting or bequeathing some/all of it – the step-up basis of CGT and CAT business relief.

- In a pension, in lots of different ways, but most clearly through the €200k tax-free and €300k standard-rated pension lump sum.

Shockingly, we only have estimates of the fiscal cost for what are likely the smallest 2 of these 6 reliefs (€430 million for CAT business relief in 2024 and €157 million for revised entrepreneur relief in 2023 according to Revenue).

But these reliefs also have wider economic costs. They create a strong set of incentives for individuals to hold assets in particular tax-favoured forms and until certain tax-favoured points in life. This distorts the choices individuals make about when and how to invest, with potentially large consequences for economic efficiency and productivity. Are we really surprised that “everyday people” – to use the Tánaiste’s term – have low rates of participation in mutual funds or ETFs when there are such enormous tax advantages to investing in one’s own home, business or pension?1

Meaningful, coherent reform of savings taxation requires addressing these distortions. It means limiting – as the 2022 Commission on Taxation and Welfare recommended – the exceptional tax advantages bestowed upon owner-occupied housing, which encourages people to invest in their home rather than companies. It means moving away from rewarding those whose business ventures have paid-off through reduced rates of capital gains tax, and towards providing upfront tax relief on new investments2 It means restricting the absurdly generous tax-free pension lump sum that primarily benefits well-paid public servants (like me!) and those with extremely large pension pots.

But meaningful, coherent, reform doesn’t seem to be on the cards. Perhaps the best we can hope for is that whatever proposals emerge from the Department of Finance over the coming months are so watered down as to be irrelevant.

1 There are also distortions created by a smaller number of tax penalties, such as the rather strange ‘deemed disposal’ rules that levies tax on ETFs “eight years after an investment is made, and every subsequent eight years, regardless of whether or not a disposal has in fact occurred”.

2 One way of doing this, suggested by Stuart Adam and Hellen Miller of the IFS in the very similar UK context, would be to align rates of Capital Gains Tax with those on employment income while introducing a pension style EET savings account for investment in new equity (like the EIIS but with full tax on withdrawals) and reintroducing CGT indexation relief (except tied to an estimate of the normal rate of return rather than the CPI). See discussion of Package 7 in their paper.